A new market study published by Global Industry Analysts Inc., (GIA) the premier market research company, today released its report titled “Active Pharmaceutical Ingredients (API) – Global Market Trajectory & Analytics”. The report presents fresh perspectives on opportunities and challenges in a significantly transformed post COVID-19 marketplace.

FACTS AT A GLANCE

What’s New for 2022?

- Global competitiveness and key competitor percentage market shares

- Market presence across multiple geographies – Strong/Active/Niche/Trivial

- Online interactive peer-to-peer collaborative bespoke updates

- Access to our digital archives and MarketGlass Research Platform

- Complimentary updates for one year

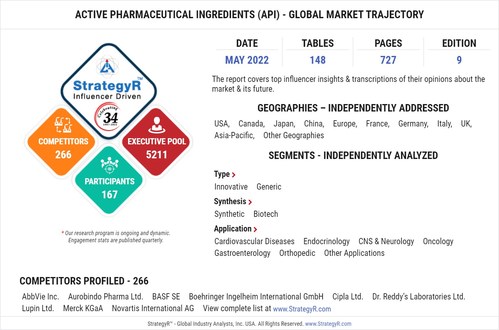

Edition: 9; Released: May 2022

Executive Pool: 5211

Companies: 266 – Players covered include AbbVie Inc.; Aurobindo Pharma Ltd.; BASF SE; Boehringer Ingelheim International GmbH; Cipla Ltd.; Dr. Reddys Laboratories Ltd.; Lupin Ltd.; Merck KGaA; Novartis International AG; Pfizer Inc.; Sun Pharmaceutical Industries Ltd.; Teva Pharmaceutical Industries Ltd.; Viatris Inc. and Others.

Coverage: All major geographies and key segments

Segments: Type (Innovative, Generic); Synthesis (Synthetic, Biotech); Application (Cardiovascular Diseases, Endocrinology, CNS & Neurology, Oncology, Gastroenterology, Orthopedic, Other Applications)

Geographies: World; USA; Canada; Japan; China; Europe; France; Germany; Italy; UK; Rest of Europe; Asia-Pacific; Rest of World.

Complimentary Project Preview – This is an ongoing global program. Preview our research program before you make a purchase decision. We are offering a complimentary access to qualified executives driving strategy, business development, sales & marketing, and product management roles at featured companies. Previews provide deep insider access to business trends; competitive brands; domain expert profiles; and market data templates and much more. You may also build your own bespoke report using our MarketGlass™ Platform which offers thousands of data bytes without an obligation to purchase our report. Preview Registry

ABSTRACT-

Amid the COVID-19 crisis, the global market for Active Pharmaceutical Ingredients (API) estimated at US$197.3 Billion in the year 2022, is projected to reach a revised size of US$250.3 Billion by 2026, growing at a CAGR of 6% over the analysis period. Innovative, one of the segments analyzed in the report, is projected to grow at a 5.7% CAGR, while growth in the Generic segment is readjusted to a revised 6.6% CAGR. The disruption and chaos unleashed by the pandemic led pharmaceutical companies to rethink their supply chains and outsourcing strategies. The pandemic’s impact on pharma supply chains was largely evident in the broken and stranded logistics as countries world over closed their borders, although late to prevent the further spread of the infection. Complete disruption and halting of the transportation and logistics sector temporarily impacted pharmaceutical drug production in countries heavily dependent on imports for active pharmaceutical ingredients (APIs). The pandemic exposed the risk of over dependence on a single country for raw materials. China supplies a lion’s share of pharma raw materials demanded worldwide. For several antibiotics and drugs, for instance drugs for treatment of high blood pressure, China is the sole source of API in the country. Over the last decade, the number of facilities in China supplying active pharmaceutical ingredients (APIs) to the U.S. alone has doubled since 2010.

Factors such as widespread lockdowns across China and airfreight disruptions heavily impacted the pharmaceutical industry, mainly in countries that rely on China for APIs and associated raw materials. The impact of stringent government guidelines on manufacturing activity resulted in a notable shortage of various APIs and related drugs in the US and other countries during the initial phases of the pandemic. Stemming from major disruptions in pharmaceutical production in China and impact on logistics, these shortages prompted India, the leading provider of generic drugs, to announce a ban on export of 26 APIs along with drug formulations. The move was intended to avoid potential shortage of medicines in the domestic market amid escalating cases of COVID-19 infection. These protectionist trade policies aimed at securing domestic pharmaceutical supplies severely undermined global equitable drug availability and access. Supply chain management over the long-term is in for some of the biggest changes not witnessed in over a century. Countries world over are encouraging pharma companies to secure themselves against volatility in supplies from Asiaand from China in particular. Some of the APIs are used for production of popular generic drugs including antibiotics and paracetamol. These restricted compounds claim 10% of India’s pharmaceutical exports and raised serious concerns in Europe and the US. Leading regulatory agencies in Europe and the US quickly sprang into actions and started closely monitoring the supply situation as any drug shortage holds serious implications for the healthcare supply chain. The entire scenario and shortage of key raw materials due to production disruptions and labor shortage indicated the heavy dependence of the global pharmaceutical industry on China for APIs. The factor has created a pressing need for pharmaceutical companies sourcing APIs from China to diversify sourcing locations and rethink the sourcing network.

While an immediate shift in pharmaceutical chemical supply lines is not a pragmatic possibility, the change is expected to gradually sink in. Spearheading the new self-sufficient sentiment in the global drug manufacturing space is India, country which is ambitiously focused on turning a crisis into an opportunity by rethinking and rejuvenating its pharmaceutical supply chain management practices and ideologies. The country’s pharmaceutical industry is currently at a very interesting stage in its evolution. By supplying massive volumes of hydroxychloroquine as a possible treatment for the COVID-19 to countries worldwide, India has emerged to become the new pharmacy of the world and is now ready for a more bigger role in the global supply hub. In addition to bold plans of capturing 5% to 8% of the global generic drugs industry, the country is also focusing on attaining self-sufficiency. In this regard, disengaging the excessive dependence on China for APIs is one of the primary areas of immediate focus. The country depends on China for over 80% of APIs needed for manufacturing drugs. In cases of certain life-saving antibiotics such as cephalosporins, azithromycin and penicillin, the dependence is as high as 95%. Initiatives are being undertaken to address supply chain issues and cost of inputs which currently remains higher when compared to imported raw materials. With countries encouraging manufacturing to return home, pharma outsourcing will be impacted. The level and severity of the impact however depends on a host of factors such as political push to bring manufacturing back home; drug regulatory changes; feasibility of re-shoring among others. In 2020, Hikal Limited, a leading manufacturer and supplier of API’s and intermediates developed Favipiravir Active Pharmaceutical ingredient (API) and its intermediates. Favipiravir demonstrated activity against influenza viruses and is approved in Japan for the treatment of novel influenza virus infections. Hikal developed this API in a record amount of time to make the product available for treatment of COVID-19.

Going forward, over the long-term, decisions to outsource manufacturing activities will be governed by more than just cost efficiency benefit. As companies emerge wiser from the lessons taught by the pandemic outsourcing drug manufacturing will mean greater focus will be shed on maintaining good reactive capacity close to where it is needed. Also, companies will now begin to outsource manufacturing to multiple countries and regions to ensure resilience in case of disasters similar to the current healthcare crisis or natural disasters. Until now, pharma companies have leveraged outsourcing as a great way to take advantage of cheap labor and raw materials available in countries like China. As the world tries to disengage dependence on China, nearshoring as a sub-set of offshoring is gaining whole new significance and reenergized focus. The closer manufacturing partners are to the home country, greater will be level of control over quality and lesser will be vulnerability to disruptions. Communication becomes easier, time-to-market is significantly reduced, chances of errors and product recalls become smaller, and control, flexibility and agility are increased x times. Vulnerability to transport disruptions also becomes significantly lower. Also nearshoring to contract manufacturers in the same time zone means lesser regulatory bottlenecks. For instance, all EU countries come under the purview of EU legislation and have similar laws related to labor and transportation. This is especially important for pharma companies which are required to maintain strict adherence to quality. Quality conformance can become a challenge outsourcing is done offshore to overseas countries like China where the laws are different. In addition to protecting against unforeseen disaster scenarios and disruptions, nearshoring also reduces quality defects, random interruptions in manufacturing processes, order processing difficulties, untimely delivery of products and mismatch between market demand and supplier responsiveness.

The emerging opportunity for nearshoring brings emerging countries like Czech Republic, Poland, Bulgaria, Brazil, Russia, Indonesia, Thailand, the Philippines, and Malaysia into the spotlight as top countries for outsourcing. These countries are also blessed with low wages, material cost, transport and travel costs and an overall conducive regulatory landscape. To encourage the opportunity governments in these countries are offering attractive tax incentives. Nearshoring is increasingly perceived to be a part of the bigger reshoring trend set into motion by the COVID-19 pandemic. In addition, to mitigate the effects of supply chain disruptions, pharmaceutical companies are increasingly recalibrated their strategies by greater insourcing and nearshoring of core products, and outsourcing non-core products and developing offshore insourcing capabilities through ‘captives’. The B2G is poised to balloon into a major trend as public-private partnerships come to the spotlight as countries initiate policy changes to bring back domestic production. More

MarketGlass™ Platform

Our MarketGlass™ Platform is a free full-stack knowledge center that is custom configurable to today`s busy business executive`s intelligence needs! This influencer driven interactive research platform is at the core of our primary research engagements and draws from unique perspectives of participating executives worldwide. Features include – enterprise-wide peer-to-peer collaborations; research program previews relevant to your company; 3.4 million domain expert profiles; competitive company profiles; interactive research modules; bespoke report generation; monitor market trends; competitive brands; create & publish blogs & podcasts using our primary and secondary content; track domain events worldwide; and much more. Client companies will have complete insider access to the project data stacks. Currently in use by 67,000+ domain experts worldwide.

Our platform is free for qualified executives and is accessible from our website www.StrategyR.com or via our just released mobile application on iOS or Android

About Global Industry Analysts, Inc. & StrategyR™

Global Industry Analysts, Inc., (www.strategyr.com) is a renowned market research publisher the world`s only influencer driven market research company. Proudly serving more than 42,000 clients from 36 countries, GIA is recognized for accurate forecasting of markets and industries for over 33 years.

CONTACTS:

Zak Ali

Director, Corporate Communications

Global Industry Analysts, Inc.

Phone: 1-408-528-9966

www.StrategyR.com

Email: ZA@StrategyR.com

LINKS

Join Our Expert Panel

https://www.strategyr.com/Panelist.asp

Connect With Us on LinkedIn

https://www.linkedin.com/company/global-industry-analysts-inc./

Follow Us on Twitter

https://twitter.com/marketbytes

Journalists & Media

Info411@strategyr.com

SOURCE Global Industry Analysts, Inc.